Trading encourages improvisation. A quick spike in the chart, a post from another trader on social media, a candle pattern that "actually looks good" - and you're trading something that wasn't even on your radar five minutes ago. This is exactly where the drift begins: away from a repeatable process and towards making decisions in line with your own emotions.

Discipline does not arise at the moment of the click, but long beforehand - in the form of rules that are so clear that they still hold under stress.

From experience, there are five levels at which rules must apply: market environment, setup, risk framework, execution and behavior. Together they form your mental foundation. If one of these levels is missing or is formulated too vaguely, your brain will find the hiding place - especially after a loss or in “periods of boredom”.

Rules reduce degrees of freedom - that's the point. A good rule catalog is not a cage; it is a filter. It removes exactly the degrees of freedom that cost you money.

Imagine two traders, both trading an opening range breakout (ORB) idea. Trader A has a “feel for the market”, Trader B has if-then rules. At 9:15 a.m. the price breaks out of the range slightly. Trader A “feels momentum” and goes long.

Trader B checks his rules: "ORB only if the first 15-minute range is at least 0.6× ATR and the breakout on a closing price basis is ≥ 0.2× ATR above the range; no execution in the twenty minutes before a news release." The breakout is too weak, news in ten minutes – no trade. In the evening, Trader A is frustrated, Trader B notes “Rules saved me from getting drunk.”

That's the core: Good rules prevent trades. Anyone who only sees rules as green lights will burn their bank accounts in difficult phases. The red light is the true account protection.

From “sounds good” to binary testable

Rules that hold are binary and measurable. “Only with strong dynamics” is not a rule. “Only if 5-minute close is ≥ 0.2× ATR above range and volume is ≥ 120% of 10-bar average” is a rule.

Your goal is to find formulations that you can tick off without any room for interpretation - and that you can validate in the MMplatinum Trading Journal. A practical approach is factorization:

- Market environment: Trend, range, volatility, event risks.

- Set up: precise entry conditions, quality levels (A/B/C), context bans.

- Risk framework: Position size, max daily loss, max trades, news blackout times.

- Execution: Order type, screenshot requirement, partial profit and trailing logic.

- Behavior: Break rules after X losses, no-trade zones, prohibited actions (e.g. postpone stop).

Formulate each rule in a way that provokes a yes/no answer. Where you would write “it depends,” there is no threshold.

A catalog of rules that saves money (using ORB as an example)

Take the popular ORB idea. Implemented improperly, it is a magnet for chance. If it is clearly defined, it becomes reproducible.

Context: "I only trade ORB on days without high-impact news in the first 3 hours after session open. Vola of the opening range ≥ 0.6× ATR of the 5-minute chart."

Entry: "Long only if 5-min close ≥ range-high + 0.2× ATR; short only if 5-min close ≤ range-low – 0.2× ATR; minimum volume = 120% of the 10-bar average."

Stop: “Initial below/above range limit −/+ 0.1× ATR.”

Management: "Partial profit 1 at +1R, rest trailing below/above structural swing low/high in 1-min chart; no adding to the position."

Invalidation: “If two 5-minute candles close against me in a row after entry and the volume falls < 80% of the average, exit to the market.”

Behavior: "After two losses in a row, 20-minute break; today a maximum of three ORB attempts."

These are not “sacred” values. They just force you to repeat the same decision chain over and over again. This is exactly what creates discipline - and with it a database that will later show you in black and white whether the setup in your instrument works.

How to translate rules into the journal (MMplatinum)

Rules without a system end up in piles of notes. In the journal they become operational:

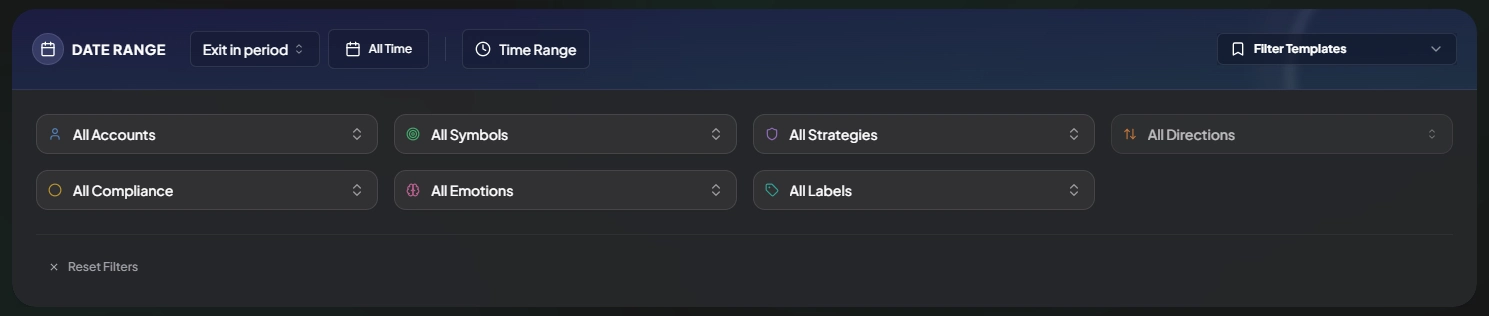

- Create “ORB M15” in the strategy Playbook and record context, entry criteria, management, invalidation, A/B/C quality.

- Use rule-based validation: Every time you enter a trade, check off which mandatory criteria you have complied with. An unchecked box is not a question of morality, but a data set.

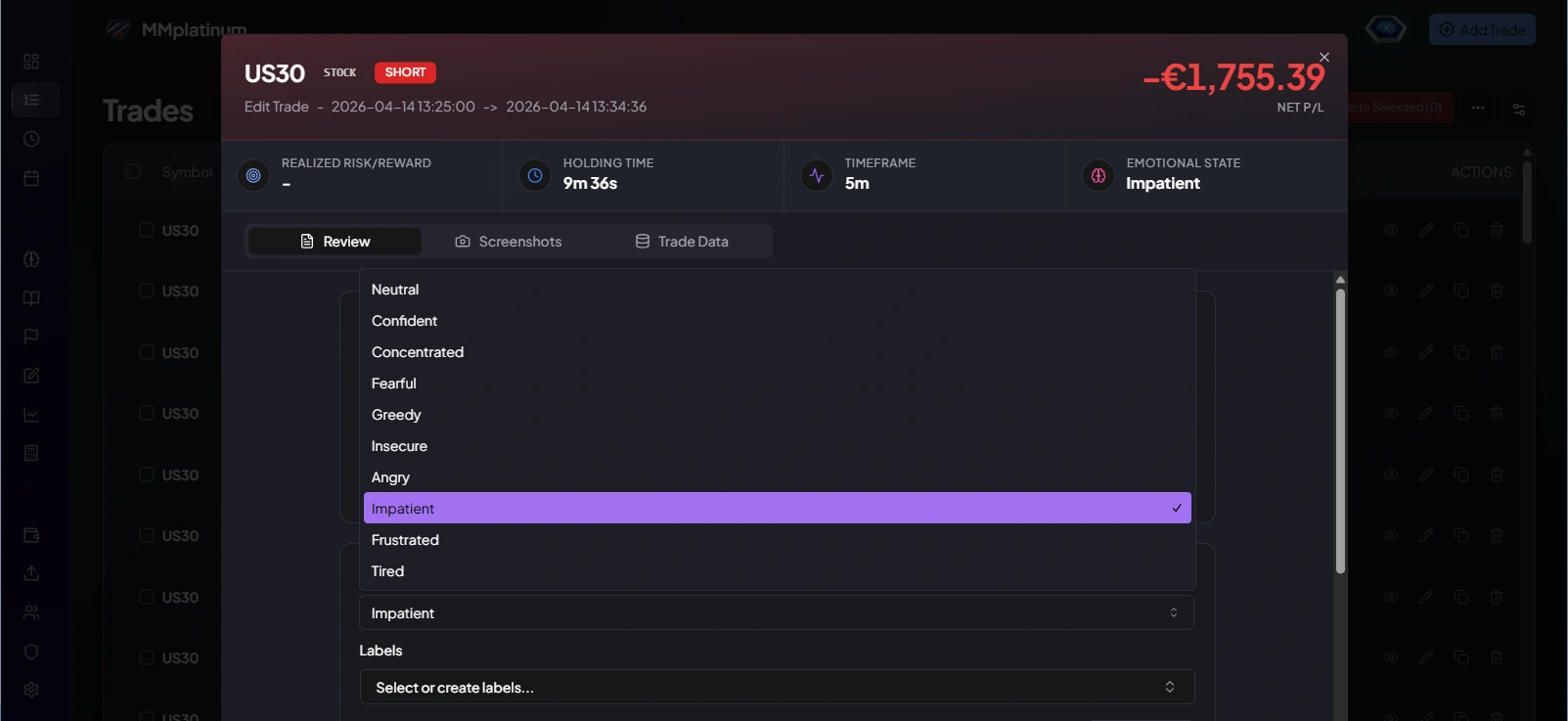

- Save screenshots as part of the execution: Entry and exit images are not optional, but mandatory. This demystifies many “it was almost an A setup” retrospectives.

- Connect the rules to your progress: The measurability of your discipline will be discussed in more detail later in the guide.

The effect is noticeable: you don't trade “intuitively”, you follow a defined process. And if you deviate from this, it is measurable - as you will read in detail later.

“Markets change” – yes. Rules too, but not every day.

A common objection to strict rules: “But markets are alive.” True. That's exactly why you need discipline to change. Rules are allowed to change - but bundled in reviews, not “on the fly” after two trades. Use Playbook versioning in the journal: changes are dated, given reasons and only become active from the coming week. This is how you separate adaptation from activism.

A practical example: You notice that in DAX futures the 0.2× ATR threshold allows for too many false signals. Instead of cranking it up to 0.3x in the heat of the moment, write down the hypothesis in the notes tab, filter the last 50 ORB trades in the journal and check the simulated effect. Only then do you adjust the rule – with the date. This approach pays off: you develop a system, not a hodgepodge of good intentions.

Micro-rules: inconspicuous but profitable

The most costly mistakes often happen between big decisions. Two examples I see frequently:

- Stop drift: After entry, the stop is pushed “a little bit” further “because the spike is sure to turn right away.” Solution: “Stop may only be moved if condition X is fulfilled (e.g. close above/below trigger bar or structure break).”

- Time window: In the afternoon your setup performs significantly worse, but you still trade it “because you have a good feeling today”. Solution: define no-trade times in the Playbook. Validation blocks you psychologically: “This setup is not allowed outside the release window.”

Such micro-rules save money because they work where willpower traditionally breaks down: in the heat of the moment.

A quick real case: same trader, different week

Monday: No rules, lots of time, two spontaneous trades, both negative. In the evening the feeling that “the market was strange”.

A week later: same setup, this time with clear rules in the journal. First breakout does not meet the rules - no trade. Second breakout fits, entry, partial win, trailing, clean exit. The difference is not in the market, but in the loyalty to the rules. The journal shows 100% adherence to the rules for the winner. You gain something that is difficult to measure and yet feels immediately: peace.

Start minimalistically, sharpen consistently

Don't start with twenty parameters that you don't know by heart. Start with the minimum that protects you: context, two hard entry thresholds, hard stop, clear management path, one invalidation, one behavioral element. Trade a series of 30-50 trades without breaking the rules. Then you do the evaluation in the journal, identify the Pareto levers, adjust one thing - and repeat the series.

This is how routine grows from rules, speed from routine, and consistency from speed. And that is exactly the currency in which this transaction is settled.

Implement in the journal: Create a Playbook for a setup today and define two red lines (e.g. max daily loss, no-trade time). Starting tomorrow: No trade without a Playbook match, no stop move without a rule condition, no review without numbers. The rest is craft.